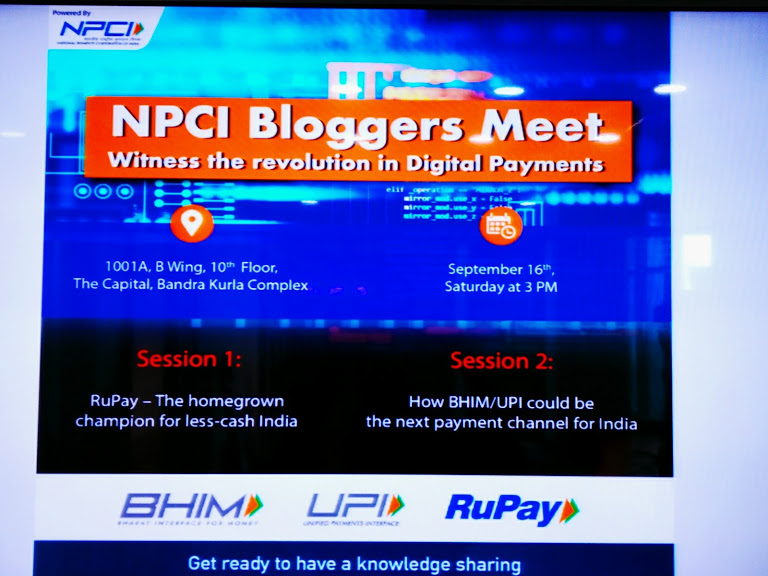

My experience was about to start with most amazing and wonderful team of NPCI and co-bloggers.

What is NPCI(National payments corporation of INDIA):

For operating retail payments and settlement systems in India NPCI is an umbrella organization, an initiative of RBI and IBA(Indian Banks Association) under the provisions of payment and settlement systems Act, 2007, for creating a robust payment and settlement infrastructure in INDIA.

NPCI has 10 core promoter banks namely, State Bank of India, Punjab National Bank, Canara Bank, Bank of Baroda, Union Bank of India, Bank of India, ICICI Bank, HDFC Bank, Citibank, and HSBC.

Marking an impacton the retail payment system over last 8 wonderful years NPCI’s RuPay is now an established brand. Recently launched products are Bharat Bill pay, National Common Mobility Card and National Electronic Toll Collection are geared to bring a new revolution in small value electronic payments.

Knowing NPCI mission of ” Touching every Indian with one or other payment services by 2020″ and a clear vision of ” To be the best payments network Globally” we all as a blogger was really keen to know what they are going to bring to us today.

It is actually One card with multiple benefits. We all carry some or other cards for the transaction so what this RuPay?

Launched in March 2012, RuPay is well poised to support the issuance of Debit, Credit and prepaid cards by banks in India and therefore supporting the growth of retail electronic payments in India.

Highlights and benefits of RuPay:

- Standardised card scheme for all banks in India.

- 380+ million RuPay cards issued by 800+ participating banks.

- Settlement in RBI accounts- no need for hedging forex risks.

- Common network, switching and interchanging fees across all banks.

- Switching fees almost one-third that of International card scheme.

- All regional rural banks and major state Co-operative banks are offering cards.

Advantages:

- All transactions under RuPay scheme are processed within the country.

- RuPay complies with the regulatory requirement for debit cards and the PIN has been made mandatory for performing any kind of transactions. This ensures a higher level of security to the customers. The approach has been endorsed by the RBI mandate on second-factor authentication for all transactions on a debit card.

- The scheme is inclusive and its rule and regulations are common across all participants.

- It’s pricing is simple, transparent and highly competitive.

- RuPay, through a dedicated relationship mechanism, works very closely with banks in helping and holding them through the onboarding exercise.

- It has a strategic tie-up with Discover financial service and Japan credit Bureau to offer international acceptance globally.

For any E-commerce service, we don’t have to do separate registration. For any transaction just need to enter card details and OTP.

What is BHIM ?

BHIM (Bharat Interface for Money) is a Mobile App developed by National Payments Corporation of India (NPCI), based on the Unified Payment Interface (UPI). It was launched by Narendra Modi, the Prime Minister of India, on 30 December 2016. It has been named after Dr. Bhimrao R. Ambedkar and is intended to facilitate e-payments directly through banks as part of the 2016 Indian banknote demonetization and drive towards cashless transactions.

The app supports all Indian banks which use that platform, which is built over the Immediate Payment Service infrastructure and allows the user to instantly transfer money between bank accounts of any two parties.It can be used on all mobile devices.

Advantages :

BHIM allow users to send or receive money to or from UPI payment addresses, or to non-UPI based accounts (by scanning a QR code with the account number and IFSC code or MMID (Mobile Money Identifier) Code).

This BHIM App is only a transfer mechanism, which transfers money between different bank accounts. Transactions on BHIM are nearly instantaneous and can be done 24/7 including weekends and bank holidays. With this app, you can check the current balance in their bank accounts and to choose which account to use for conducting transactions, although only one can be active at any time.

This BHIM App is only a transfer mechanism, which transfers money between different bank accounts. Transactions on BHIM are nearly instantaneous and can be done 24/7 including weekends and bank holidays. With this app, you can check the current balance in their bank accounts and to choose which account to use for conducting transactions, although only one can be active at any time.

If the 12-digit Aadhaar number is listed as a payment ID, the BHIM app will not require any biometric authentication or prior registration with the bank or Unified Payment Interface (UPI).

*99# and it’s just simple with any mobile phone.

After knowing about this app I have downloaded it and used and trust me it’s worth to have this app in your mobile and make life easy and worth.

If in simple language I explain about this app so it would be ..

”

WigglingPen elaborate it little further and define it as a wrapper of all the Banks who are associated with BHIM. Isn’t tricky ??? Let me explain you….the whole idea of UPI is to bring the convenience for today’s consumer. Imagine in last 10 years you are managing your 4 bank account and now you have 4 mobile app to deal it with each bank……. Difficult!!! Isn’t ?? Remembering 4 account IDs, 4 password….saving your password in your mobile ….risky !!!

Here NCPI helps you to share your burden by giving you a Unified Payment Inferface i.e. UPI.

It’s the most convenient way to transact across Bank. What you need to do is just download the mobile app – BHIM from any of your playstore and map your bank account to that. Interestingly the moment you map you account to BHIM it will make a skin of your bank account and it will act as if it is your mobile Bank app. In case you have 4 bank accounts, you map all and make anyone as a default account and start transacting thru that. It’s secure and trusted way to do your transactions. Happy Banking

BHIM app currently supports 12 languages (including English), though there are totally 22 of the official languages of India (excluding English) under 8th Schedule of Constitution of India.

With NPCI, wigglingpen also believe that yes one day this revolution will change the face of transactions in INDIA.

{kind=link}

{kind=link}

This looks like you had a great informative session at the meet up. This organization has made digital transactions safe for us.

With so many supposed solutions these days, it is difficult to know whom to choose and use. This post is definitely helpful as it explains about the product and its features and benefits.The fact that it supports all indian banks is definitely an advantage.